A comprehensive macro-economic assessment analyzing the systemic vulnerabilities of the Russian Federation’s wartime economy as of mid-2026. This report examines the decay of strategic trade alignments, the domestic crises shaking the defense industrial base, the artificial overcooling of consumer demand, and the escalating turbulence within the banking, energy, and corporate sectors.

The Illusion of Sino-Russian Economic Synergy and the Sino-Siberian Gas Stagnation

The structural relationship between Moscow and Beijing has faced significant reassessment following recent bilateral diplomatic summits. While state-controlled media apparatuses continue to project an image of uninterrupted economic synergy, deep-seated protectionism and divergent long-term strategic plans have introduced visible friction into the alliance.

The Structural Death of the Power of Siberia 2 Project

The long-heralded negotiations surrounding the construction of the “Power of Siberia 2” gas pipeline have fundamentally stalled, exposing the limits of China’s reliance on Russian raw energy exports. For years, the Kremlin framed this project as an absolute replacement for the lost European natural gas market. However, internal corporate strategic shifts within Beijing indicate that China has no logistical or economic necessity for the pipeline.

China’s newly enacted five-year economic blueprint allocates massive state capital to the domestic expansion of renewable energy infrastructure, specifically wind and solar installations. Concurrently, Chinese energy corporations have unlocked substantial internal shale gas reserves, drastically expanding domestic extraction. Consequently, China lacks the structural import capacity to absorb an additional 50 to 100 billion cubic meters of Russian gas, leaving the Power of Siberia 2 as a defunct project in the eyes of international energy analysts.

Agricultural Protectionism and the Poultry Ban Scandal

The underlying competitive tension between the two nations manifests not only in the energy market but also in direct trade disputes that are routinely minimized in public communiqués. Immediately prior to high-level state visits, Russia’s agricultural oversight agency, Rosselkhoznadzor, enacted a sudden sweeping prohibition on poultry imports originating from China, citing the discovery of dangerous bacterial pathogens.

Independent analysis reveals that this scientific justification was primarily a protectionist maneuver designed to pacify domestic agricultural syndicates. Throughout the first quarter, Russian domestic poultry producers suffered a sharp contraction in manufacturing output, prompting an intense lobbying campaign to shield the domestic market from cheaper Chinese imports. This administrative dispute demonstrates that Beijing operates primarily as an aggressive market competitor rather than a benevolent economic ally to Moscow.

The Currency Paradox: How a Strong Ruble Destroys the Russian Defense Sector

The financial mechanisms governing the Russian ruble have generated a highly paradoxical economic environment. While state propagandists point to the currency’s nominal appreciation against Western denominations as a validation of economic resilience, industrial leads view this development as an existential threat to manufacturing stability.

The Machine Builders Congress and Chemezov’s Warnings

The systemic damage inflicted by the volatile exchange rate was explicitly articulated during the recent Machine Builders Congress, a major summit uniting Russia’s heavy industrial and defense manufacturing leadership. Sergey Chemezov, the influential head of the state-owned Rostec defense conglomerate, along with various directors of major military-industrial enterprises, delivered a series of blunt assessments regarding the current state of industrial profitability.

They testified that the rapid over-appreciation of the ruble — which temporarily drove the exchange rate below 70 to 74 rubles per US dollar — has directly eroded the financial viability of the military-industrial complex. The strength of the national currency has severely inflated the internal production costs of military hardware, rendering Russian defense exports deeply uncompetitive on the global market, particularly when contrasted against heavily subsidized alternative equipment manufactured by Chinese enterprises.

However, this inflated revenue stream remains fundamentally unsustainable, as soaring energy costs are rapidly accelerating global “demand destruction.” As detailed in market reports highlighting how the Strait of Hormuz shutdown triggers oil ‘demand destruction’ as families and businesses ditch gas, both households and commercial enterprises worldwide are aggressively cutting consumption and abandoning traditional fuel, ensuring that Russia’s temporary petrodollar windfall will soon collapse under a sharp contraction of international market demand.

The Incurable Onset of Wartime Dutch Disease

The artificial inflation of the ruble is a classic manifestation of Dutch Disease, supercharged by regional geopolitical crises. The escalating conflict in the Middle East and the prolonged disruptions in the Persian Gulf have driven international crude oil prices upward, resulting in a massive, concentrated influx of petrodollars into the Russian financial system.

This narrow revenue surge strengthens the currency on paper but leaves the broader, non-extractive manufacturing sector completely exposed. During the industrial congress, when executives pressed the executive branch for direct interventions to suppress the ruble and slash the central bank’s astronomical interest rates, the political leadership responded by advising the assembly “not to speak of sad things.” This public evasion highlights a profound deadlock between short-term political posturing and long-term industrial survival.

Monetary Hyper-Emission and the Artificial Subcooling of Domestic Demand

The financial leadership of the Russian Federation is struggling to balance massive federal military expenditures with the preservation of macroeconomic stability. The reliance on raw monetary printing to sustain the invasion of Ukraine has triggered a defensive, highly disruptive reaction from the state’s fiscal regulators.

The Double-Velocity Explosion of M2 Money Supply

A granular review of Russia’s monetary aggregates reveals the true driver behind the state’s highly publicized gross domestic product growth metrics. Analytical reports verify that the domestic M2 money supply has experienced an unprecedented hyper-emission cycle since the commencement of the full-scale invasion of Ukraine.

By April 2026, the volume of circulating currency in the Russian economy skyrocketed from its pre-war baseline of approximately 60 trillion rubles to an astonishing 132 trillion rubles. This means the money supply now represents nearly two-thirds of the nation’s entire GDP, whereas it previously accounted for less than half. The 4% annualized economic growth frequently boasted of by the Kremlin is entirely an artifact of this massive monetary injection, which is concentrated strictly within the defense industrial apparatus and does not reflect real wealth creation.

Nabiullina’s Miscalculation and the Demand Depression

The Central Bank of Russia, led by Elvira Nabiullina, has attempted to counter this structural inflationary pressure by deploying an aggressively restrictive monetary policy, keeping interest rates at historic highs. The declared objective of this strategy was to delicately cool consumer demand, aligning it with the country’s actual productive and investment capacities.

However, external data indicates that the central bank failed to execute this transition. Instead of a controlled stabilization, the combination of extreme borrowing costs, international sanctions, and military monetary distortion has pushed the economy through the “thin ice” of stability. Consumer demand has been pushed into a deep depression, leaving domestic non-military manufacturers with expanding stockpiles of unsold goods and an acute lack of purchasing consumers.

The Chasm Between Official Deflation and Real Consumer Price Hikes

The macroeconomic slowdown has led to misleading public data, with state statistical organs heavily promoting short-lived windows of weekly deflation, tracking price drops as low as 0.02%. However, internal bulletins published by the central bank confirm that these localized price dips are entirely temporary, driven primarily by intense administrative pressure applied by the Federal Antimonopoly Service to artificially suppress the cost of basic seasonal fruits and vegetables.

In sharp contrast, the core service sector — which accurately reflects persistent inflationary pressures — remains locked at an annualized inflation rate of 10.9%. Furthermore, the central bank’s own public surveys reveal that the population’s observed inflation rate stands at a critical 15.1%, exposing a profound chasm between simulated state statistics and the real-world reduction of consumer purchasing power.

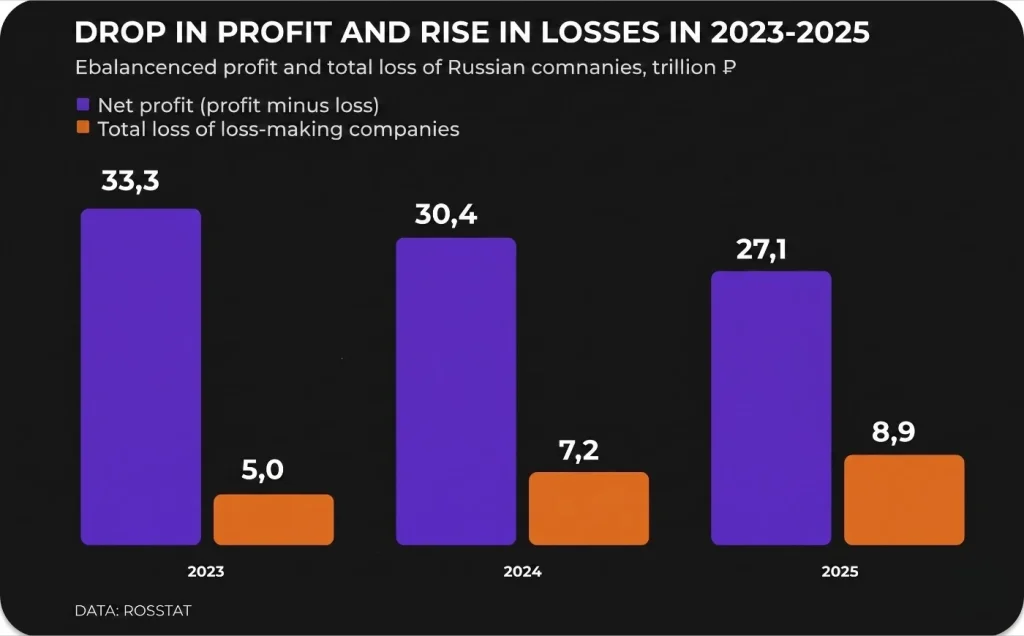

Structural Insolvency: Cash Gaps, Metallurgy Collapse, and Hidden Bankruptcy

Beneath the surface of state-funded production pipelines, the Russian private sector and heavy raw materials industries are facing a severe systemic cash crisis. High interest rates have made standard corporate credit lines inaccessible, preventing companies from smoothing over routine operational friction.

The Nationwide Proliferation of Severe Corporate Cash Gaps

According to specialized financial audits published by domestic business journals such as Vedomosti, over 53% of all registered Russian corporations and individual entrepreneurs have experienced severe, prolonged cash gaps throughout the current fiscal year. Critically, a quarter of these enterprises reported experiencing these liquidity emergencies for the first time in their operational histories.

A corporate cash gap occurs when an enterprise incurs immediate manufacturing and operational debts but faces extensive delays in receiving final payments from buyers. In a functional economic system, these short-term discrepancies are mitigated by routine bank financing. At current interest rates, however, borrowing to cover operational gaps is financially ruinous, leading to a cascade of non-payments across major commercial supply chains.

The Hidden Bankruptcy of a Third of the National Economy

The exponential accumulation of corporate losses indicates that between 25% and 30% of the entire Russian economy is currently operating in a state of functional, hidden insolvency. This structural decay encompasses an economic value estimated at roughly 50 trillion rubles of the national GDP.

These enterprises are no longer capable of generating net profits or independently covering their operational overhead. They remain afloat solely by delaying payments to suppliers, hoarding raw materials, and maintaining an unsustainable reliance on anticipated state subsidies. Because the federal budget is increasingly monopolized by direct frontline military expenditures, these sweeping corporate bailouts are structurally impossible, making the formal liquidation of a vast swath of the civilian economy merely a matter of time.

The Collapse of Domestic and Export Metallurgy

This insolvency crisis is acutely visible within the metallurgy sector, which traditionally served as a pillar of industrial stability. In April, domestic steel production in the Russian Federation suffered a sharp contraction of nearly 8% in annualized terms, while general domestic metal consumption plunged by 15% across the first quarter.

This drop is directly linked to Russia’s complete displacement from traditional Western export markets and its inability to compete on remaining international routes. Russian metallurgical combines have found themselves systematically priced out by cheap, state-backed Chinese steel filling the global market, turning a historical industrial asset into a loss-generating sector.

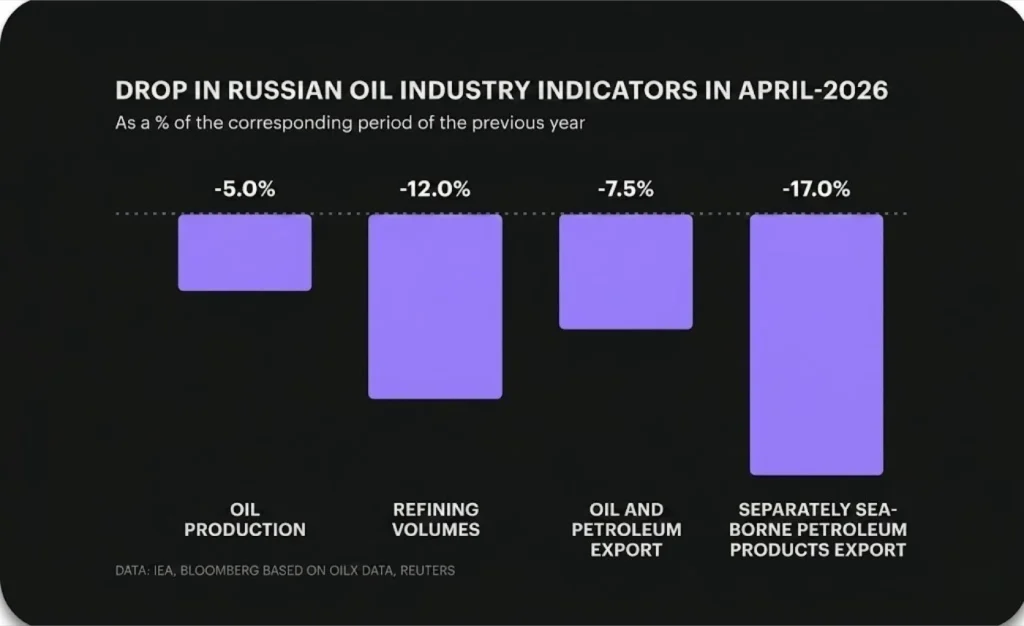

Fuel Crises and Refinery Attrition: The Tangible Impact of Long-Range Interdictions

The physical infrastructure powering Russia’s primary export engine and domestic agricultural logistics has become a focal point of vulnerability. Sustained asymmetric long-range interdictions executed by Ukrainian forces have begun to reshape the internal distribution and processing metrics of the national energy sector.

Systemic Contraction of Processing and Maritime Export Metrics

Despite concerted administrative efforts by the Ministry of Energy to suppress infrastructure data, consolidated international shipping and refining registries confirm deep structural damage across the sector. By the close of the spring season, Russian domestic oil refining volumes suffered an annualized contraction of 12%, representing a total drop of 20% when measured against the pre-war baseline of early 2022.

Furthermore, total maritime exports of refined petroleum products — principally heavy fuel oil and diesel — fell by 17%. While crude oil extraction dropped by 5% in annualized terms, the state managed to temporarily stabilize macro-revenues by routing raw, unrefined crude to alternative international buyers. This tactical shift, however, strips the state of the high profit margins associated with domestic refining, turning Russia back into a raw extraction economy.

Exchange Restrictions and Regional Rationing

The domestic fuel market is showing clear signs of strain. In the wholesale sector, the volume of gasoline offered on public commodity exchanges has dropped to a three-year minimum, as major oil corporations increasingly hoard refined product to meet mandatory domestic quotas. This supply squeeze has caused wholesale diesel prices to surge on national exchanges, while retail fuel prices have steadily climbed by 4% since the start of the year, consistently outstripping official inflation metrics.

The regional impact is most acute along the critical logistics nodes of the southern front. In occupied Crimea, local administrative authorities have been forced to implement strict rationing, officially prohibiting the unrestricted commercial sale of fuel and capping consumer distribution at 20 liters per individual. This localized rationing underscores the high vulnerability of the state’s energy supply lines to targeted long-range interdiction campaigns.

Consumer Destitution: Microfinance Surges and Regulatory Pushback in Personal Bankruptcies

As the civilian corporate sector contracts and real inflation diminishes the baseline value of working-class wages, the Russian population is increasingly turning to high-interest debt mechanisms to sustain routine household expenditures.

The Three-Year High in Debt Collection Transfers

During the first quarter, the volume of personal and consumer debt formally transferred by credit institutions to third-party collection agencies climbed to an absolute three-year high, approaching a total value of 400 billion rubles. Crucially, statistical audits of the credit market reveal an unprecedented structural inversion: for the first time in the history of the modern Russian banking sector, the volume of defaulted debt originating from microfinance organizations (MFOs) surpassed standard commercial bank loan defaults.

Microfinance entities specialize in short-term, predatory loans issued at exorbitant interest rates to individuals lacking the creditworthiness required by traditional banks. The fact that MFO debt now dominates collection pipelines demonstrates that the poorest layers of the Russian population are completely exhausting their financial reserves to cover basic living costs.

The Insolvency Surge Among Individual Entrepreneurs

A parallel crisis is unfolding within the entrepreneurial sector, where the number of individuals formally filing for judicial bankruptcy has risen to 137,000 cases in the first quarter alone, representing a 14% annualized increase. This insolence surge is concentrated heavily among individual entrepreneurs (IEs), a category that witnessed a 30% explosion in formal bankruptcies.

These small-scale businessmen have been hit simultaneously by escalating federal tax brackets, mandatory social contribution increases, and the sharp drop in civilian consumer demand. Unable to secure affordable credit or sustain baseline sales volumes, thousands of independent operators are forced into total financial liquidation.

Administrative Restrictions on Total Debt Discharges

To prevent a complete unraveling of the consumer credit market, state judicial authorities have implemented aggressive administrative measures to limit access to bankruptcy protection. Russian courts have significantly tightened criteria for total debt discharge, resulting in a threefold increase in formal rejections issued to applicants seeking debt relief.

While the state continues to formally register individuals as bankrupt to satisfy statutory requirements, the judiciary increasingly refuses to legally liquidate their outstanding liabilities. Debtors are left legally labeled as bankrupt while remaining fully responsible for servicing their loans to state-linked banks, an administrative block designed to protect the liquidity of major credit institutions at the direct expense of the population.

Geopolitical Externalities: Sanctions Erosion and Global Macroeconomic Volatility

The structural outcome of Russia’s internal economic crisis remains closely linked to wider geopolitical transformations and shifting regulatory policies across the Western hemisphere.

The Persian Gulf Crisis and Sanctions Dilution

The prolonged military gridlock in the Middle East and the persistent blockade of the Strait of Hormuz have inadvertently provided the Kremlin with temporary diplomatic leverage. Fearing a global energy price spike that could trigger a wider Western economic recession, several major economies have quietly eased enforcement of their restrictive regimes against Russian energy exports.

The United States extended its specialized maritime exemptions for the transport of Russian crude, while the United Kingdom enacted a broad, open-ended authorization permitting the domestic import of aviation fuel and diesel processed from Russian crude within third-party nations, such as India. Concurrently, Valdis Dombrovskis, the European Commissioner for Trade, explicitly acknowledged that the G7 coalition currently lacks the diplomatic consensus required to lower or further tighten the $60 oil price cap mechanism, highlighting how international energy anxieties continue to blunt the efficacy of targeted sanctions.

Federal Reserve Transitions and Global Recessionary Risks

The broader international investment community is displaying heightened anxiety regarding structural global inflation. Yields on United States Treasury bonds have experienced a sharp upward trajectory, climbing to levels not witnessed since the global financial crisis of 2007.

This macro-anxiety has been amplified by the installation of Kevin Warsh as the new Chair of the Federal Reserve, a leadership transition that has introduced considerable policy uncertainty. With domestic United States inflation tracking at nearly 4% due to the ongoing maritime crisis in the Middle East, international markets are bracing for the prospect of aggressive interest rate hikes under Warsh’s tenure. Such a tightening cycle threatens to push the global economy into a synchronized recession, an eventuality that would rapidly suppress international demand for crude oil, dismantle Russia’s temporary petrodollar windfall, and accelerate the structural collapse of the Kremlin’s heavily overextended war economy.

This analytical report was compiled based on the economic briefing and data analysis provided by Vladimir Milov on Michael Nacke’s channel →